Nevada Area Play, Golden Lake - GLM, SALT

Potential 10 Bagger

Welcome and thank you to all the new, smart, savvy and contrarian investors to my substack. If you like outside the box thinking, a humble analyst that has spent his career studying market and economic cycles, picked numerous tops and bottoms, someone not afraid of controversial topics and can be a bull and a bear, your at the right place.

Kirkland Lake Gold was the most successful gold stock in the past decade, expanding through acquisition to an intermediate. Then their acquisition of Newmarket Gold that owned the Fosterville project in Australia drove the stock bonkers, to over $50 in August 2020.

In February 2022 Kirkland Lake was merged with Agnico Eagle. Kirkland shareholders ended up with 46% of the merged entity that was valued at US$22.4 billion the day of the merger representing a value of about US$10.3 billion for Kirkland Lake. And today under Agnico Eagle, Fosterville ranks as their 2nd highest grade mine at 8.1 g/t for proven and probable reserves with total ounces of 1.4M

I followed Kirkland Lake closely and was planning on a report on the company, but I was waiting for a pull back in the stock, it just seemed too high compared to many other mid size gold stocks. In hindsight we know the stock never pulled back an appreciable amount, it just kept going higher.

So where did the founders of Kirkland Lake end up? In 2021 they started a junior called North Peak Resources TSXV:NPR. In May 2023 North Peak acquired their Prospect Mountain Mine complex in Nevada's Battle Mountain Eureka trend.

North Peak CEO is Brian Hinchcliffe co founder of Kirkland Lake, Mike Sutton Director was also a co founder of Kirkland Lake with Mr. Hinchcliffe and Harry Dobson an Insider of North Peak. And John Thompson, Director of North Peak was the CFO at Kirkland Lake.

On August 14th North Peak released first assay results from the continuing drilling at the Prospect Mountain North area of its Prospect Mountain property

Drill Hole PM24-004 opened up potential for mineralization throughout the Wabash and Williams historical drilling area as it was almost completely mineralized, intersecting 415 feet (126.49 metres) of 1.06 grams per tonne gold and 12.3 grams per tonne silver from zero feet, which included 40 feet (12.19 metres) of 4.20 grams per tonne gold and 71 grams per tonne silver from zero feet.

Since then, the stock moved up from around $0.90 to $1.15. I am considering the Stock for the newsletter but it has considerable resistance around $1.25. I want to see it break above that or fall back down below $0.90.

However, what is important, that virtually no investors know of and what could be a huge opportunity, is North Peak's property is smack in the middle of Golden Lake's Jewel Ridge property claims and furthermore some of North Peak's drilling is pretty much on the border of Jewel Ridge.

Golden Lake TSXV:GLM, OTC:GOLXF

Strong buy to Cdn8 cents

Shares Outstanding – 83 million - 52 week trading range $0.04 to $0.10

Golden Lake and their Jewel Ridge property, has about 1/8 the value of North Peak, giving a potential for a 10 bagger.

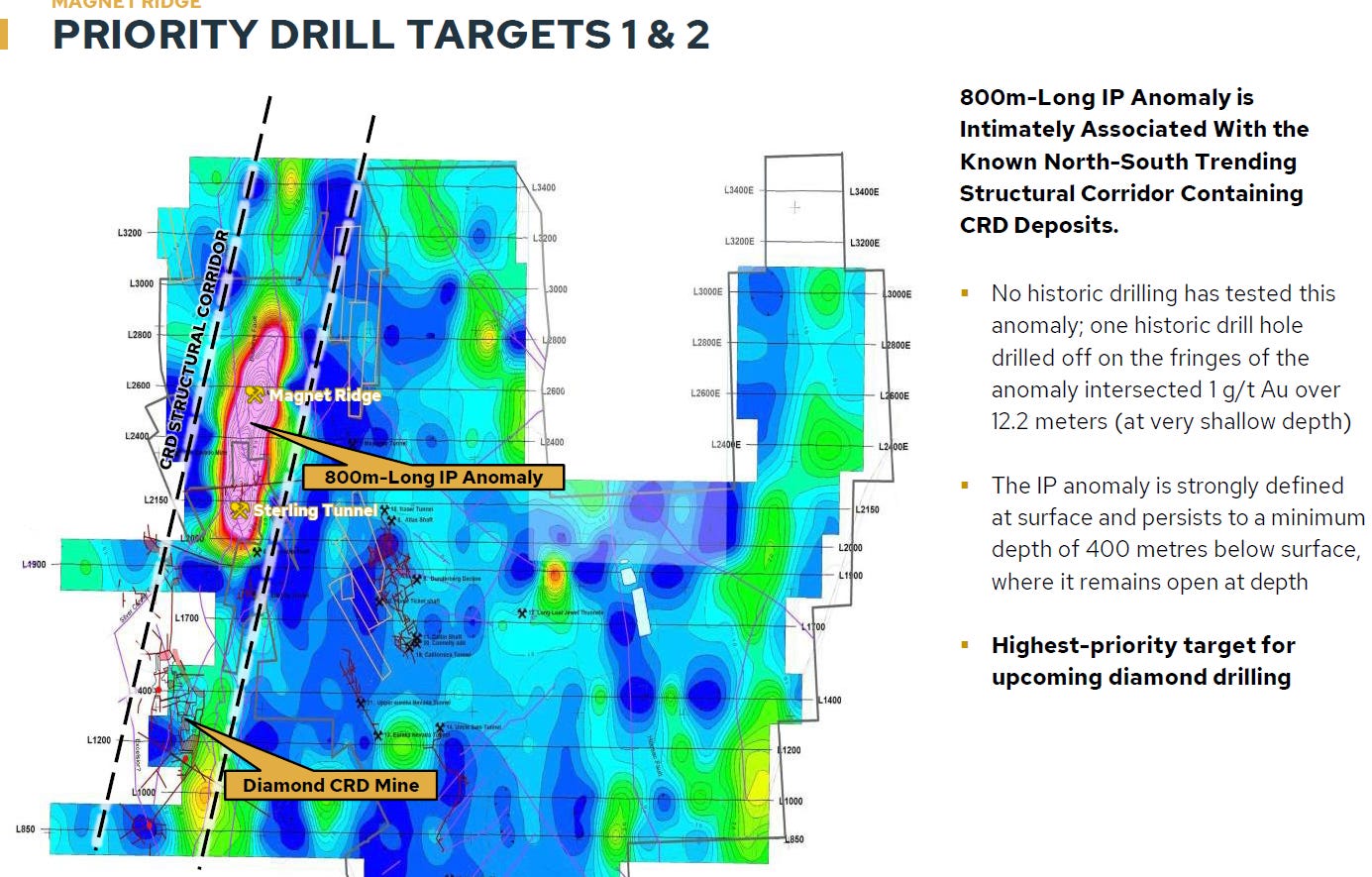

On the map below, the CRD Deposits are aligned in a north-south trend over 10km from the Ruby Deeps, Hilltop deposits to the north on 1-80 ground (green) to the Diamond/Excelsior deposits to the south, North Peak ground (kind of beige). GLM's Jewel Ridge is yellow highlighted in red.

These deposits are all related to a north-south fault complex. The Magnet Ridge target (black oval) is situated in the heart of the corridor and comprises an untested 800-metre-long IP anomaly.

North Peak Drilling is at the bottom of this IP anomaly.

Further more McEwen Mining just acquired junior Timberline Resources for about $25 million for their Eureka property above and below Golden Lake's Jewel Ridge.This area is smoking hot, McEwen just paid 5 times the value of GLM for Timberline and I believe GLM has a better property, but has not had enough drilling yet.

When I asked Mike England the CEO of Golden Lake, why the stock is so low. His comments were that right now we are the forgotten junior.

This is a closeup and shows better detail. North Peak is getting good results and they are not even in the strong spot of the anomaly in pink.

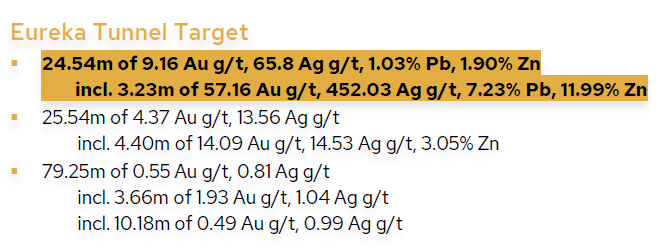

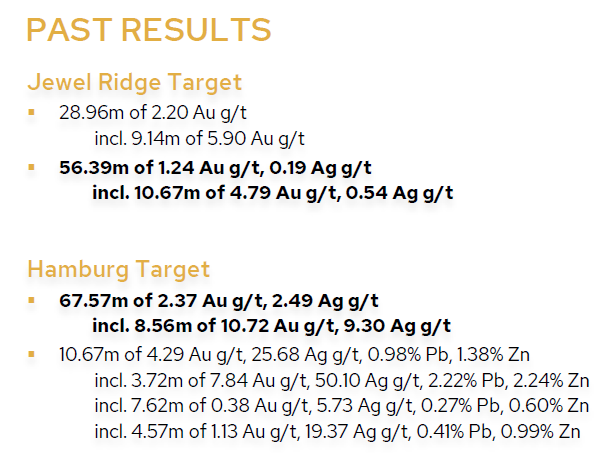

Now, it is not like this is virgin ground because there are many historic drill holes with great numbers. And also good drill intersects from Golden Lake's previous drilling. Here are some of these. Eureka Tunnel Target is to the right of the IP anomaly.

The Jewel Ridge and Hamburg Targets are in the bottom portion of the claims near Timberline, now McEwen Mining's Windfall project.

On August 19th, GLM announced that The Bureau of Land Management (U.S. Department of the Interior) has approved Golden Lake's plan of operations, authorizing preparatory and certain exploration activities, including diamond drilling, to be undertaken on Golden Lake's flagship Jewel Ridge property, located in the prolific Battle Mountain-Eureka gold trend of Nevada.

"The plan of operations is a big asset for Golden Lake moving forward. We are very excited to get drilling our first four priority, deeper targets at Jewel Ridge, which to date has seen only shallow holes over the years," commented Mike England, Golden Lake chief executive officer.

Conclusion

The property is well located proximal to infrastructure and is immediately adjacent to successful, high-profile exploration programs currently being undertaken by both i-80 Gold Corp. and North Peak Resources Ltd. on their neighbouring Ruby Hill and Prospect Mountain properties, respectively. And McEwen Mining will get active here, now that they bought out Timberline.

In my August 20th update on gold, I had a lot of detail on the record M&A activity in mining with 643 deals in 2023. Never in history has there been so many deals involving junior exploration companies with no resources and often little drilling and/or small historic resources. It is continuing into 2024 with McEwen's acquisition of Timberline just one example from dozens.

It is because never in history have junior explorers been this cheap relative to their assets. That is changing and will be fast - as 100s of these little juniors go under or get bought up, the investment pie gets smaller and smaller. I predict the rest of this year and next will be the biggest ever for junior explorers regarding return to investors, The TSX Venture index around 560 would give about a 100% return just to get back to the 2021 highs when gold was only $2,000 per ounce.

Golden lake is an obvious take over target for i-80 Gold, North Peak and now McEwen Mining. If any one of these offered 15 to 20 cents per share, in this market shareholders might go for it. Lets hope that doesn't happen because I think GLM could get up to $0.50 to $1.00 on good drill results.

Golden Lake's upcoming drill program at Jewel Ridge is timely, in view of the encouraging drill results recently announced by North Peak at Prospect Mountain.

North Peak reported the results from the first 10 holes of its 2024 reverse circulation drill program targeting the Wabash/Williams/Silver Connor historical mine areas (see North Peak's news release dated Aug. 14, 2024). Many of the drill holes completed by North Peak, among them PM24-004 and PM24-006, are situated within 200 metres from the western boundary of the Jewel Ridge property. Drill hole assays include:

1.06 grams per tonne gold and 12.30 g/t silver over 126.5 metres (including 4.20 g/t Au and 71.00 g/t Au over 12.2 metres) in drill hole PM-24-004;

1.38 g/t Au and 26.32 g/t Ag over 35.1 metres (including 2.03 g/t Au and 38.26 g/t Ag over 21.3 metres) in drill hole PM-24-006.

And to top it off, the chart looks quite good. We definitely have a bottom with a triple test in the 4/5 cent area. You can see it has been in a 3 year down trend like most all junior explorers, but it appears it is breaking out of this down trend and a wedge pattern. There is some resistance around 8 cents and a break above that would confirm a new bullish trend with a higher high.

*************** Updates **************

Atlas Salt - - - TSXV:SALT - - - - - Recent Price $0.70

Entry Price $0.58 - - - - - Opinion – buy on weakness

So far it looks like we picked a bottom pretty close to get back in. This week SALT entered into a non-binding memorandum of understanding with Scotwood Industries LLC to establish a strategic salt production offtake agreement and joint venture for the distribution and sale of packaged salt and related products in Canada.

The non-binding MOU does not include the sale of bulk road de-icing salt, and excludes the provinces of Newfoundland and Labrador, Prince Edward Island, New Brunswick, and Nova Scotia, subject to certain exceptions with respect to national accounts and expansions of existing relationships that Scotwood has with retailers in the United States that have Canadian affiliates doing business in those provinces.

The joint venture would target annual sales volumes for the strategic offtake and distribution of products of 1.25 million to 1.50 million tonnes per annum, subject to market conditions.

About Scotwood Industries LLC

Scotwood is an industry leader in the marketing and distribution of salt products in the United States, operating since 1980. Scotwood is the largest packaged retail de-icing distributor in the United States, with a loyal customer base, including leading big box mass merchandisers, do-it-yourself, farm and home, grocery, hardware, and automotive chains, with existing relationships averaging over 20 years.

The business would take advantage of Scotwood's deep industry and client expertise, and Atlas Salt's long-life, low-cost, proximal supply to strategically serve the Canadian retail market for the distribution and sale of products. A very good deal for SALT and will help move the project forward.

Paid Advertisers at playstocks

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.