Perfect Bad Timing & sell NKTX +200%

Struthers Report V30 # 1. 2 with CPE takeover

I expect 2024 will be a much better year for the junior miners and we will see some big gains. I had some questions, why I have stuck with Zonte so long and still bullish.

Zonte Metals - - - - TSXV:ZON - - - - -OTC:EREPF - - - -Recent Price - $0.08

Entry Price - $0.09 - - - - - Opinion – buy

This chart is the history of Zonte trading since it started to trade in October 2010. The stock had almost the perfect bad timing. It came out trading and rose like gangbusters because we were in a strong bull market for precious metals and the mining stocks. Zonte caught the tail end as the precious metals market peaked in the first half of 2011. It has been a down market since and in fact the worst bear market in history for precious metals mining stocks. Zonte started out at $0.16 and currently at $0.08 is down -50%

I would have liked to get this comparison with the TSX Venture index on the same chart but could not find a way to do so. This next chart is the TSX Venture index over the exact same time frame and it has dropped from about 1,800 to the current 549 or down -70%. Zonte did much better than the market and probably 95% of other junior explorers. Since 2011, there are maybe half a dozen to a dozen junior explorers that made a discovery and their stock is closer to breaking even or a small to decent gain. For example, Blackrock made a very good discovery and we bought the stock at $0.14, it ended the year at $0.32, simply pathetic. This one got started in 2016 after most of the market decline.

In 2011 at the market top we sold out of a whopping 17 stocks that year for average gains of 228% yes it was very good. However by year end, the miners were tanking with many junior explorers down -40% to -80%. Zonte was down -51% at year end.

After that is was all bad as you can see from the chart above there was hardly a rally until 2016 and we did manage to sell for some profits after that.

In 2018 sold Garibald GGI +733% and Jaxon JAX + 74% - Zonte was up 107% at that time

In 2019 sold RJX Exploration RJX.A +140% - Zonte was up +120% at that time.

Well that is all history and does not matter any more. History is good to learn from but one of the biggest mistakes investors make is projecting history into the future. Here are some examples:

This 40 cent stock was $5 two years ago, it could go back up there;

This stock has done nothing and gone no where the last 3 years, why should it change;

The last two time this stock went up, it fell right back again.

One thing that history is good for with stocks is on the chart. It is sort of investors trading on emotion based on their historical experience. There are resistance levels at price points on a chart where there was a lot of trading. For example on Zonte's chart above there will be resistance around $0.20 because it traded a lot around that price in 2020 and 2021.

Here are emotions that effect investors. They are disgusted and bearish the stock dropped from $0.20 to $0.06 so to satisfy their emotions they tell themselves that they are selling as soon as it gets back to $0.20 and they are even again.

Stocks go up and down because markets change, fundamentals change and investors change their perceptions. After such a long wait, I believe things are going to change for Zonte this year. After a lot of work, Terry Christopher has figured out Mother Natures secrets at Cross Hills. Let me explain and some good education on copper deposits. First a look at the top three copper bearing minerals.

You can find pure native copper and that is what the ancienst mined back in the bronze age. Modern science has come a long way since then. Chalcopyrite, a sulphide mineral is the most common copper mineral and contains about 34% copper by weight.

Bornite - a sulfide mineral that contains up to 63% copper by weight. It is often found in association with chalcopyrite and is a secondary source of copper production.

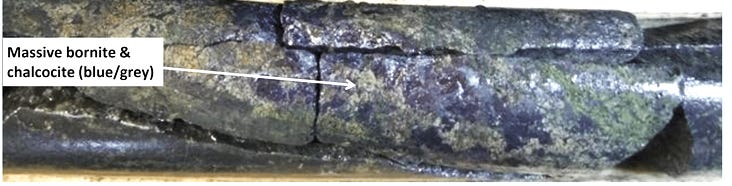

Bornite with chalcocite was the mineral found in Zonte's high grade drill core a few years ago that ran 14% copper with 15 g/t gold and 352 g/t silver. Here is the pic of that drill core.

Now hold on to your hat. I want to show you what is important about all this black you see in Zonte's drill core. It is Chalcocite, a secondary copper mineral that forms from the weathering of primary sulfide minerals, such as chalcopyrite. It contains up to 80% copper by weight and is an important source of copper in some deposits.

Next pic of Zonte's drill core from late 2023, note the core box that is second from the bottom, it has some good sections with a lot of black. This is Chalcocite, the mineral that carries the highest grade of copper.

Chalcocite is the highest grade copper mineral and that is what you see in this drill core. That said, we don't know if there is enough chalcocite distributed throughout the core for high grade assay results. There is no telling for sure if we see 0.2% copper over many meters or 15% copper. We have to wait for assays.

Regardless, it is my believe a discovery will be made when these results come out. Keep in mind that K6 that was drilled here is one of the smallest and not among the best targets either. However, it was a very attractive target and the most advanced to drill ready in this IOCG system.

I recently watched a video by an Australia expert on IOCG systems. He noted that one importance of IOCG systems is that they are typically higher grade copper than other copper deposits and that they can be very large.

I know some of you will think that you have heard these positive type things before, but it is very important to keep in mind that exploration is a process. Some deposits are harder to find than others and I often use the famous Hemlo gold discovery in Ontario that was not found until drill hole number 76. The late Murray Pezim that financed the play was persistent and would not give up. Don McKinnon was one of the three prospectors that made the discovery and he was a subscriber to my newsletter for many years.

Terry Christopher has been as persistent as Murray Pezim but did not have the deep pockets as Pezim in his day, so Christopher's persistence is better measured in years and meticulous geological work than Pezim's dollars spent.

I will also note that John Kaiser, a newsletter with a huge following started coverage on Zonte in late 2023. He was not real bullish but more like it is on his watch list. So I surmise if Zonte does make a discovery there will be a lot of new buying and the stock does have a large following, it has just not been an active one, like most junior explorers. At current prices, there is a lot more upside than downside. I like the risk/reward setup.

Nkarta - - - - - - NASDAQ:NKTX - - - - - - Recent Price - $9.40

Entry Price - $3.12 - - - - - - - Opinion – sell

NKTX went over $10 this morning on heavy volume, about 14 million by 11:30 AM. This looks like the short squeeze that I though should happen, so we should sell into this. When the short covering is over it will probably come back down.

Callon Petroleum - - - - - NY:CPE - - - - - -Recent Price $34.50

Entry Price - $41.62 - - - - - - - Opinion – buy

I last commented on CPE with a buy in November at $32.20 and talked about how cheap it was, well, I guess APA Corporation agreed.

Last Thursday a buyout of Callon was announced. APA Corporation (NASDAQ: APA) and Callon Petroleum Company ("Callon") (NYSE: CPE) have entered into a definitive agreement under which APA will acquire Callon in an all-stock transaction valued at approximately $4.5 billion, inclusive of Callon's net debt. Under the terms of the transaction, each share of Callon common stock will be exchanged for a fixed ratio of 1.0425 shares of APA common stock. The transaction is expected to be accretive to all key financial metrics and add to APA's inventory of high quality, short-cycle opportunities. Callon's assets provide additional scale to APA's operations across the Permian Basin, most notably in the Delaware Basin, where Callon has nearly 120,000 acres. On a pro forma basis, total company production exceeds 500,000 BOE per day and enterprise value increases to more than $21 billion.*

Key Highlights

Combination of Callon's Delaware-focused footprint with APA's Midland-focused footprint provides scale and balance in the Permian Basin;

APA's oil-prone acreage in the Midland and Delaware Basin combined will increase by more than 50% following the transaction;

Expected to be accretive on key financial and value metrics;

Estimated overhead, operational and cost-of-capital synergies to exceed $150 million annually; and

Additional scale anticipated to improve credit profile; pro forma balance sheet will remain strong with leverage at 1.1x net debt / adjusted EBITDAX.**

I expect CPE could work out much like Earthstone did for us where the combined larger company gets a higher valuation in the market, so I would hold CPE and take the APA shares. And with oil down today, I see CPE as a good buy.

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.