PPI ok, Millennium Index, B2Gold BTO, GSPR

Option Speculation List

The NFIB Small Business Optimism Index rose by 3.4 points in December to 105.1, the second consecutive month above the 51-year average of 98 and the highest reading since October 2018. I would think a lot of this is some high hopes with the new Trump administration that is generally more favourable for business, but there will be a lot of economic challenges for Trump and his gang.

There was no big deal with producer prices reported today, but the bad news will be in the months ahead. The producer price index for final demand rose 0.2% last month after an unrevised 0.4% advance in November. Economists polled by Reuters had forecast the PPI climbing 0.3%.

In the 12 months through December, the PPI accelerated 3.3% after increasing 3.0% in November., the biggest jump since February 2023. Higher energy was to blame and since oil and gas prices jumped higher - so January's number could be high. Core PPI was unchanged from November but up 3.5% on the year.

Yesterday, I mentioned about power line maintenance and PG&E causing L.A. fires. News is out now that residents and business have launched a lawsuit against Edison Int. for improper maintenance of power lines that caused the L.A. Eaton Fire. Not proven yet but no surprise.

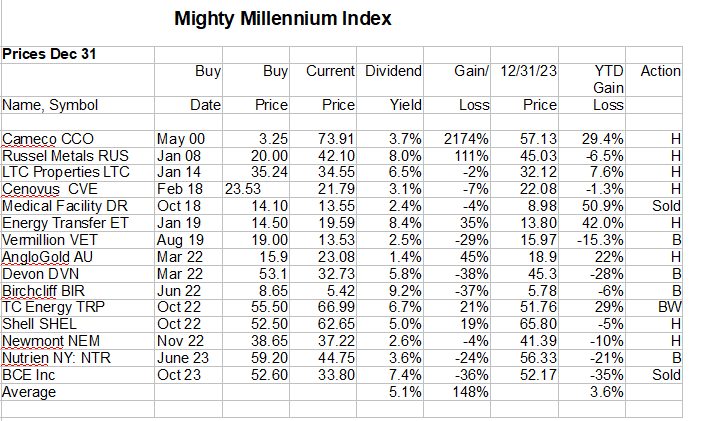

The index had a mediocre year but I have set it up to do well in good or poor years. The return was 8.7% with dividends and the most negative impact on the index was the weak and under valuation of our oil&gas stocks and a badly timed buying of BCE Inc. The oil&gas stocks have already started a decent recovery.

The major change I am making for now is I am adding B2Gold to the index because it is way over sold and currently has a dividend yield of 3.3%. I am then going to sell AngloGold on a recovery back to around $30, as it has a lower dividend and in fact the lowest dividend on the list. We ended up with AngloGold shares when they bought out Centamin CEE that had a high dividend.

B2Gold - - - TSX:BTO, NY:BTG - - - - Recent Price - $3.55

Entry Price - $4.45

Opinion – strong buy, average down to $3.90, Stop/loss - $3.30

Yesterday B2Gold announced total consolidated gold production for 2024 of 804,778 oz, within their guidance range. Total gold production for 2025 is anticipated to be between 970,000 and 1,075,000 oz. The Goose Project remains on track for first gold in Q2 2025 and total capital estimate remains at C$1,540 Million.

The expected increase in gold production relative to 2024 is predominantly due to the scheduled mining and processing of higher-grade ore from the Fekola Phase 7 and Cardinal pits made accessible by the meaningful deferred stripping campaign that was undertaken throughout 2024. Also the expected contribution from Fekola Regional starting in mid-2025, the commencement of mining of higher-grade ore at Fekola underground, and the commencement of gold production at the Goose Project by the end of the second quarter of 2025. These will be partially offset by the scheduled conclusion of open pit mining activities at the Otjikoto Mine in the third quarter of 2025.

B2Gold’s initial Goose Project life of mine plan to be released at the end of the first quarter of 2025 based on updated Mineral Reserves. The Company continues to estimate that gold production in calendar year 2025 will be between 120,000 and 150,000 ounces and that average annual gold production for the six year period from 2026 to 2031 inclusive will be approximately 310,000 ounces per year, with the latest published Mineral Reserves supporting a long mine life beyond 2031.

I have shown this slide from their presentation before that shows significant production growth in 2025 and will be more so in 2026 with a full year at Goose. Delay in permitting at Fekola caused the production drop, this is resolved now and there will also be a big drop in AISC (costs) for 2025.

I am showing the US$ priced chart, symbol BTG because most trading is U.S. and with the drop in the C$ (loonie) it can cause different technical s on the chart that are more currency related than trade related.

In October the stock did not quite break out and it has corrected way more that most gold stocks. I cannot think of any good reason other than some funds sold making year end adjustments. Whatever, it caused a triple bottom at year end with a strong bullish up candle the first of January. Currently you get about a 6.4% dividend yield while we wait for the stock to recover. At this time B2Gold is my favourite gold producer and I would also consider Call options.

I would go with the U.S. January 2026 $3 Calls at $0.35

on the Canadian side the September $4.50 Call for $0.30.

There is not near as much volume and open interest on the Canadian side so why I picked September, at least it has some open interest. I would favour the U.S. options, but I will add both on our speculation/option list.

I am also doing the 2024 review of last years options.

With options, timing is everything and we did manage a decent gain of +48% thanks to some big gains like the Newmont call options but our gold stock options in the first part of the year did not work out as the gold stocks badly lagged gold and continue to do so but not quite as bad as early in 2024. It seemed the option picks did either very well or very bad. For 2025 I plan quicker profits and taking part profits early.

I became more cautious and suggested fewer options and recently longer dates. Since year end our MRNA Put is doing much better, but the PanAmerican Silver PAAS January $20 Call expires on Friday and it last traded at $0.70. Like many gold and silver stocks it got whacked at year end. Lets see if we get a bounce up in gold yet this week and try to close this Call around $1.50. It was up near $2.00 Monday for a while.

Option List for Paid Subscribers

GSP Resources - - - - TSXV:GSPR, OTC:GSRCF - - - Recent Price - $0.12

Entry Price - $0.15 - - - - - - Opinion -buy

GSPR announced initial results for the first hole of 7 diamond drill holes targeting potential extensions of known high grade copper and gold zones at their Alwin Property, B.C.

Drill hole AM-24-01 intersected multiple zones of high-grade copper-silver-gold mineralization over a combined 36.2 metre (m) core interval. Significant assay results include a main zone averaging 2.41% Cu, 35 g/t silver (Ag), and 0.68 g/t gold (Au) over 17.4 m , including 4.11% Copper, 60 g/t Ag and 0.95 g/t Au over 8.4 m ; in addition to an upper zone grading 1.01% Cu and 10.7 g/t Ag over 5.5 m.

This is a very good intersect for the first drill hole reported. We should see more the same in upcoming results from the remaining 6 drill holes completed during the 2024 drill campaign that are pending and will be released in the coming weeks as they are received.

This drill hit is below the historically mined area and within the planned pit perimeters.

Simon Dyakowski, CEO of GSP commented , “We are excited that the first drill hole of our Q4 2024 drill program has yielded broad zones of high-grade copper accompanied by consistent silver and gold values. Our initial mineral resource estimate for the Alwin Project was well received by the market and we believe these exceptional initial drill results are a direct result of our deepened understanding of the mineralization controls at Alwin. We look forward to releasing additional positive drill results in the days and weeks ahead, with an eye to in-pit resource expansion, new discoveries, and evaluating the high-grade gold potential of the Project. We are also pleased to have completed the 100% acquisition of the project on an accelerated timeline, with a simplified and less burdensome cash and share outlay and NSR structure.”

The market for junior explorers is still weak but the stock jumped to 14 cents on the news and is back down to 12 cents, still unable to crack that 13 cent resistance. A good buy level and next results may easily get the stock through unlucky 13.

Paid Advertisers at playstocks

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.