Silver Break Out confirmed, Buy Coeur Mining CDE, Sell NKTR

Welcome and thank you to all the new, smart, savvy and contrarian investors to my substack. If you like outside the box thinking, a humble analyst that has spent his career studying market and economic cycles, picked numerous tops and bottoms, someone not afraid of controversial topics and can be a bull and a bear, your at the right place. Please share and subscribe.

Silver is up again today, currently $34.72 up about $0.64. This confirms yesterdays breakout and if you remember back in April or early May, I highlighted the breakout from a cup and handle formation and that would lead to a major upside move. This is not confirmed and I see $50 as the near term target.

Similar to gold, investor participation is still quite low. Volumes into the silver etf SLF are up some but no where near 2020 volumes. There are all kinds of silver bullion available at the coin dealer I use.

Our silver stocks are not dragging down the average performance of our gold stocks as much now and I would like to add another one to the list.

Coeur Mining has been a laggard in this bull rally thus far because it is not well understood. Investors seem to remember more of their legacy than who they are today. Many investors know Coeur as a silver company, but for many years now most of their revenue and profits is from gold. Around $7.20 the stock is well below it's 2021 highs around $11.50 and 2016 highs of $16

Coeur Mining - - - NY:CDE - - Shares outstanding 399 million

In Q2 2024 Gold sales were US$154.1 million and silver sales were $67.9 million. This makes gold sales almost 70% of revenues. The stock should have responded more to the rising gold price, but as I said, I think investors were still viewing Coeur as mostly a silver company.

That said, they do have large leverage to silver because their resource base they are almost 60% silver. The Company is maintaining its full-year production guidance ranges of 310,000 - 355,000 gold ounces and 10.7 - 13.3 million silver ounces. Full-year CAS guidance at Palmarejo and Wharf have been reduced to reflect strong cost management efforts, while Rochester’s second half CAS guidance ranges have been increased to reflect timing of ounces placed under leach.

Other significant news on the silver front was just a couple weeks ago on October 4. Coeur announced that they entered into a definitive agreement to acquire all of the issued and outstanding shares of SilverCrest pursuant to a court-approved plan of arrangement.

Under the terms of the Agreement, SilverCrest shareholders will receive 1.6022 Coeur common shares for each SilverCrest common share. The Exchange Ratio implies consideration of $11.34 per SilverCrest common share, based on the closing price of Coeur common shares on the New York Stock Exchange (“NYSE”) on October 3, 2024. This represents an 18% premium based on 20-day volume-weighted average prices of Coeur and SilverCrest each as at October 3, 2024.

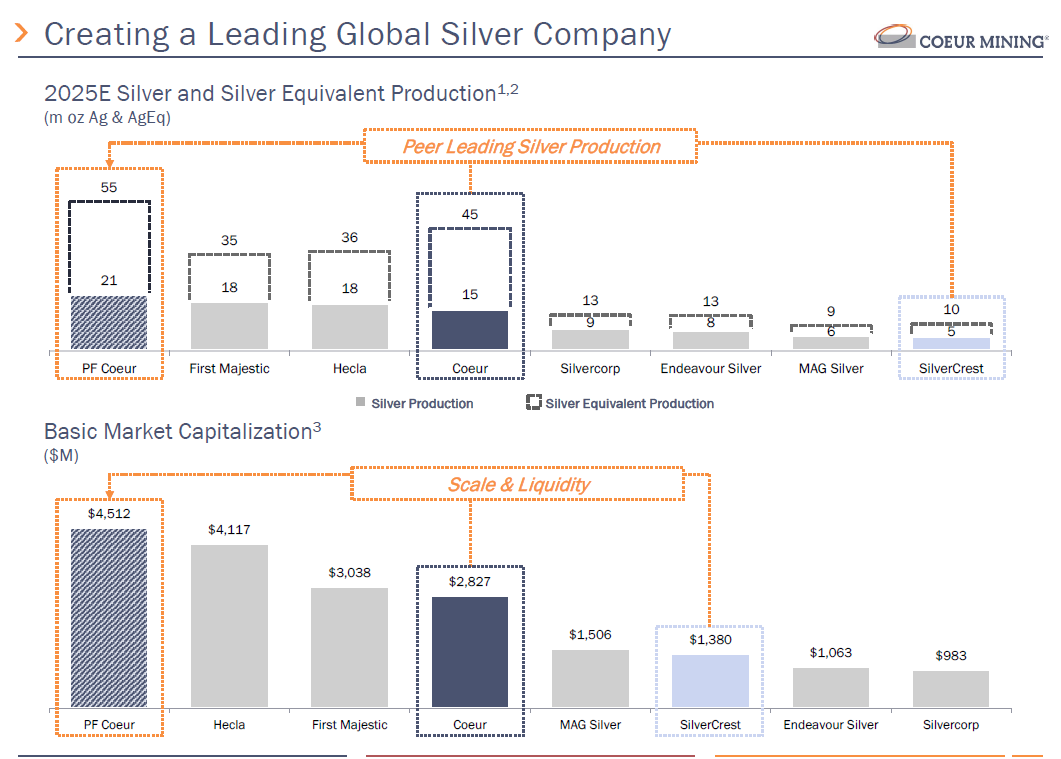

It turns out, this was a very well timed acquisition ahead of the silver price rise and it will make Coeur the world's largest pure silver producer at about 21 million ounces per year. Their silver production should be neck and neck or just a little behind Pan American Silver not shown on this graphic.

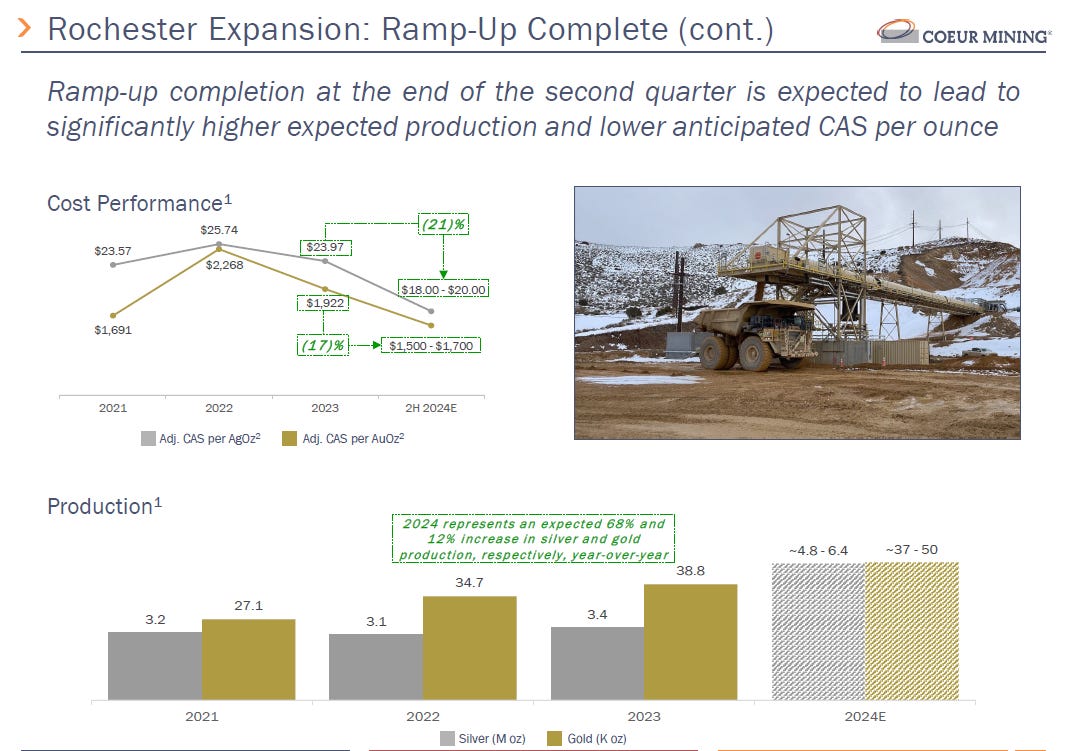

Another key positive fundamental is the expansion of their Rochester Mine this year. Mid September they announced that the new three-stage crushing circuit continues to deliver greatly enhanced levels of flexibility to accommodate the full range of mined ore at Rochester. For the month of August, approximately 2.7 million tons were placed on the new Stage VI leach pad, representing a 39% increase over July placement levels. Rochester remains on-track to place 7.0 – 8.0 million tons per quarter during the second half of 2024 and to achieve its full-year 2024 production guidance of 4.8 – 6.6 million ounces of silver and 37,000 – 50,000 ounces of gold.

Rochester is the largest open pit heap leach operation in North America and largest silver reserve asset in the U.S.

At the end of 2023 Coeur had 3.2 million ounces of proven and probable gold reserves and 243.9 million ounces silver. At the long term reference of 60 to 1 ratio, their reserves are 58% silver and 42% gold.

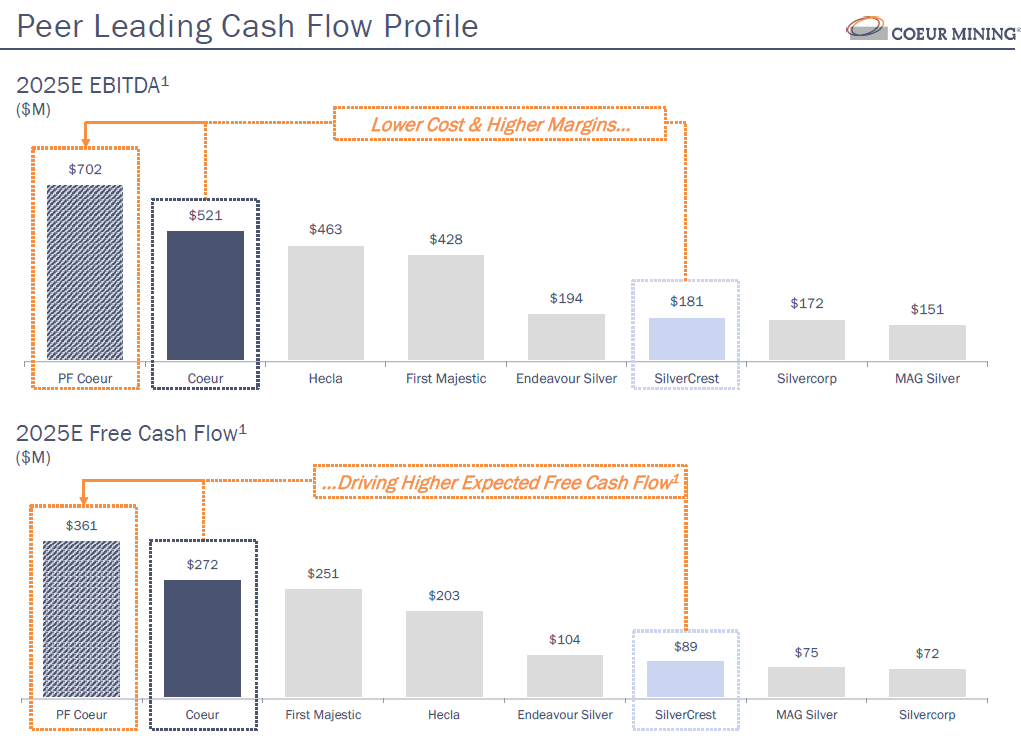

With the significant expansion at Rochester and the acquisition of SilverCrest it will make a significant positive effect to increased profits and cash flow. According to Coeur's presentation, using Factset Street Research data, they will be the leader among peers. The Pro Forma adding SilverCrest is significant. The higher silver price is more gravy on top.

The chart looks good too. Volume is picking up and looks like the stock will break through the resistance area and head to $11.

You can get some more leverage with Call options Because this is a low priced stock, I would take advantage of low premiums on long dates. The December 2025 $5.50 Call option is about $2.75 and is $1.87 in the money so a premium less than $1.00 for almost 14 months.

Nektar Therapeutics - - - NASDAQ:NKTR - - - Recent Price $1.41

Entry Price $0.68 - - - - - Opinion – sell

There is nothing wrong with the company, but I am concerned we could get a significant market correction and I don't like the fact the stock has not done better in a bullish market. That said, I think this reflects how concentrated this bull market is and does not have good breadth. The stock is just below cash value but the stock is near resistance on the chart and besides that we have over 100% profits in about 8 months, lets take them.

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.