Hope is not a Plan, Stagflation and Oil Breakout

Struthers Report V29 #3.7 - Greenbriar

Market narrative goes along the line that inflation will ease back to 2% and interest rates will do the same. I have been harping that we are in a period of stagflation like the 1970s, which means slow growth and high inflation.

We could see a recession this year and it will likely not bring down inflation. The theory is that a recession will bring down demand. However, since most of the inflation is from the supply side, it means that demand may have to be reduced drastically to be effective. Hoping for lower inflation and interest rates is not a good investment plan. For today's report, I will show why this is just hope and touch on three things that will make the current high inflation very sticky.

First the US labour problem, worker shortage is structural. This means a tight jobs market and pressure for high wages that will help fuel inflation will be around for many years.

Edward Dowd is a highly successful market analyst and very good number cruncher. He was much like me in regard to the experimental shots. We have both followed bio-tech companies and know it takes 7 to 10 years to prove any drug or vaccine safe and effective. After a drug/vaccine makes it past animal trials, less than 10% are brought to market and FDA approved. We both took a wait and see position, let others try it and see what happens. In hindsight we now know the shots were neither effective or safe.

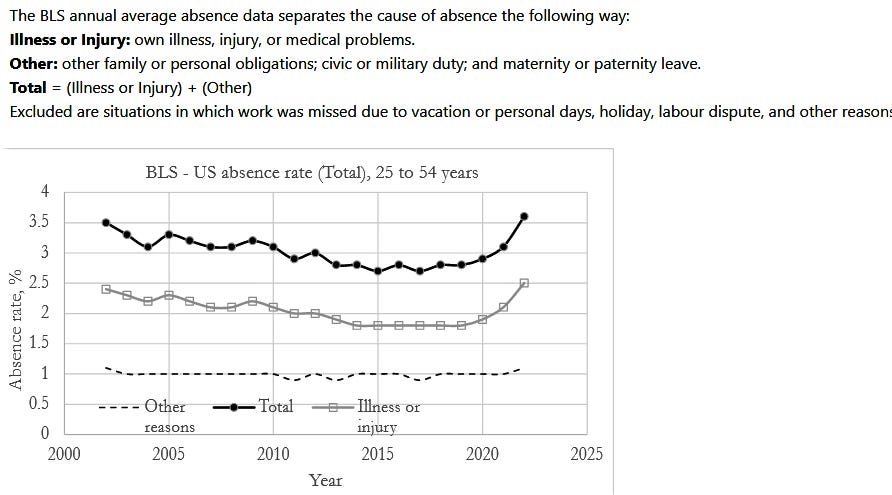

Mr. Dowd crunched recent and historic numbers out of the monthly jobs reports, the BLS data. The results were astounding. Illness, injury and medical problems rocket launched in 2021 and 2022. We all know what was different in those two years, the experimental shots.

There was a general declining trend in total absence rates from 2002 to 2019. This was driven by the decline in absence rates due to illness or injury, as the rate of other causes of absence remained almost constant throughout the period. From 2020, absence rates due to illness and injury rose substantially, in particular in 2021 and 2022, while absence rates for other causes remained the same.

Mr. Dowd created many charts in part 2 of his analysis. I present just two here.

This reveals that there was more than 11 standard deviations with is huge. I tried to find the odds of 11 deviations and found tons on the math but not a simple table on the odds. I know it would be 1 in 10s of millions, maybe billions?

There was not much of an increase in 2020 and certainly an increase would be expected with the onslaught of Covid-19. The huge jump in 2021 and 2022 can only be one thing in my opinion.

Regardless, the important point is that there is over 3 million people extra (above the norm) out of the work force due to illness, injury or medical problems. This is a significant number and it does not look like it will resolve itself soon.

In this next chart you can see that Baby Boomers are well into their retirement age in 2021 compared to 2009. Covid-19 and all the restrictive government policies caused many boomers to throw in the towel and retire earlier when they might have worked a few more years into their retirement age. These workers are not coming back and many more will be retiring.

A very severe recession will be needed to bring the jobs market back to an equilibrium. Furthermore, due to supply chain issues in recent years governments and many corporations have changed policies to bring more manufacturing and jobs back to the US. It is not hard to conclude that rising wage pressure will continue. This chart from Statista shows wage growth has gone up to 6% and appears to be levelling here. In Canada the Federal Minimum Wage Rising to $16.65 per Hour on April 1st. In both Canada and the US we have tax and spend governments that are only adding to inflation.

Second - Energy Prices along with number three, government policy

High energy prices were a major factor driving inflation higher in 2022 and also a major factor bring it down. I believe energy prices will go back up because of government policy against fossil fuels while they promote green energy. I believe in green energy but energy security should come first. This green energy thing is a whole new topic, but suffice to say, governments will screw up the transition to this. As the chart below shows, US Energy Inflation has pretty much reversed all of the 2021 and 2022 gains. The trend is most likely to go up some and certainly it is less likely more reductions will help ease inflation further.

In Canada, Trudeau's recent budget increased carbon taxes 30% from $50 to $65 per tonne. This relates to about 3 cents per litre increase in gasoline and 17 cents per litre for diesel fuel as well as increases on your home heating bills. Once again inflationary policies from government.

With government policies against oil&gas companies and the previous exploration incentives and credits removed, can you blame these companies from no longer trying to grow production and sending returns back to shareholders? These drilling numbers should be no surprise.

Fed Drilling Survey Shows Drastic Drop. The US oil and gas activity survey published by the Federal Reserve Bank of Dallas indicates that activity stalled in Q1, with the index plummeting from 30.3 in the fourth quarter of 2022 to 2.1 currently amidst rising field costs, higher interest, and plunging gas prices.

War is not only a factor in curtailing oil& gas supply like the destruction of Nord Stream pipelines but it also increases the use of fossil fuels to power a war machine. You can be certain that Russia and Ukraine are using much more fuel. The US military uses about 200,000 barrels per day oil equivalent in peace time. If the Ukraine war escalates as it looks to and/or China soon mobilizes against Taiwan, a huge increase in energy consumption would result.

We are really at war, but many do not realize it. I was not surprised at all with the OPEC news today but markets were, and shocked by the oil output cut from major producers in the OPEC+ group. WTI crude futures (CL1:COM) surged past $81 a barrel at the open to its highest price since late January, with the May contract rallying as much as 8%. US foreign policy has been a disaster and I have commented before that the Saudis were more likely to align with eastern block countries over the west. The Saudis have recently taken steps to join the Shanghai Cooperation Organization, invested billions of dollars in Chinese petrochemicals, and even turned to Beijing to broker a normalization deal with Iran.

The output reduction will be led by OPEC kingpin Saudi Arabia, with total production cuts totalling nearly 1.2M bbl/day - that will start in May and last until the end of 2023. Russia's recent production cuts of 500K barrels per day were also extended, and add to the 2M bpd that were taken offline by OPEC+ in October.

It appears oil prices might have broken their down trend. However, I am still watching the $82 level I pointed out some months back. We need to see a solid close above $83 for solid prove the down trend is broken. I also like the fact the oil market had a wash out as one or more of the failed banks was forced to liquidate, as I commented on my substack a week ago or so.

There was huge news today on a stock I own and follow that makes it very unique and probably a first in a new trend.

Greenbriar - - - TSXV:GRB - - - OTC:GEBRF - - - Recent Price - $C1.10

Greenbriar is the first public company in North America to have certain registered common shares alternatively listed as digital shares on the INX. This means that potential shareholders without a brokerage account can buy Greenbriar shares through a digital wallet like they do with Crypto currencies. These are typically smaller investors and you could have millions of them owning 5 to 20 shares.

The tokenized version of the Greenbriar shares will be subject to the same benefits afforded to the existing registered and non-registered shareholders, which includes voting rights and a share of the company's profits in the form of dividends. The digitized shares are easily tradable since they can be bought and sold 24/7/365 on the INX.One digital asset platform. Plus, these shares, like all security tokens available on INX.One, are Finra approved securities. INX Securities, a broker dealer, is a SEC Finra approved broker/dealer and Alternative Trading System ("ATS"). Digitization or Tokenization is not available to Canadian residents because INX is not a registered broker-dealer in Canada.

Here are a few comments from the news release -

"By working with INX, Greenbriar and certain Greenbriar registered shareholders, we will be able to begin to offer a Finra approved, secure and direct pathway for financial markets to unlock another source of possible liquidity through the INX ecosystem," said Itai Avneri, Deputy CEO & COO of INX. "As the first Finra approved digital asset platform to achieve regulatory approval to raise capital, issue security tokens and trade both security tokens and digital currencies, it's an exciting next step for INX to offer the first digitized shares of a publicly traded company to both U.S. and international investors. It also marks a significant inflection point in the maturity of the digital economy."

"We are thrilled to be taking these essential steps to be the first public company in North America to have certain registered common shares alternatively listed as digital shares on the INX. One security token platform," said Jeff Ciachurski, CEO of Greenbriar Capital. "I am delighted to say, INX is a Finra approved platform merging investing and trading in security tokens, cryptocurrencies, and capital raise services all in one platform. Greenbriar deeply believes in the full democratization of investing. Rather than limiting the expansive opportunities of Greenbriar to just our existing 3,000 to 4,000 public shareholders, owning on average 8,000 to 9,000 common shares each; through digitization we can dramatically increase access and the number of public token holders - providing ownership opportunities to everyone in the worldwide security token ecosystem. All security tokens digitized from registered common shares will have full voting and dividend rights."

Greenbriar will lock up an initial arm's length current common registered shareholder (and in time, future registered shareholders after the initial registered shareholder) and their common shares into an escrow account with the Computershare. Subsequent to this, INX will then mint the one-to-one equivalent amount of the security tokens and then deliver them to the initial registered shareholder who will have an INX Securities, LLC account, who in turn will then be allowed to trade security tokens on the INXS ATS. This process can be repeated with additional shareholders as market liquidity for the tokens increase over time.

Up to 100% of the issued common shares are available to tokenize, provided however that all of the shareholders owning such shares would be non-Canadian residents. The Company has no way of determining who exactly is a legal Canadian Resident at any given time, therefore the exact percentage is unknown. The cost to tokenize is up to $8,000 per month for more than 5,000 token holders but only $2,000 per month for up to 500 token holders. The tokenization process is a cost to the company. In addition, there are initial set up and listing fees totalling CDN $40,000.

In 2021, INX became the first SEC-registered digital security IPO - closing with $84 million in gross proceeds from over 7,250 retail and institutional investors. 92.9 million INX Tokens were sold in the IPO. INX continues to lead the industry in providing novel trading and capital raising financial instruments to enterprises and companies worldwide.

In time this is going to create much more demand for Greenbriar shares and with that higher prices. Regardless the stock is trading at it's lows on this 3 year chart, so down side risk appears small.

I would also like to thank and welcome the 300 plus that have joined my substack thus far.

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication