Trump's Big Deal, Tariffs, Stagflation, Housing and Rents Plunging

My Gold Picks

The changes under the Trump administration are going to be very disruptive and there will be short term pain. I think it could work in the long run, time will tell. Canadian media is full of propaganda on these tariffs. Simply put, Trump won a historic election on his America first policies and is implementing what he said he would do. For decades, Canada has been sucking off the U.S. tit as far as trade goes while keeping heavy protection measures on many Canadian industries. Many experts I respect say if you read Trump's book 'The Art of the Deal' you would understand this better.

Trump is positioning America to negotiate better terms in the North America Free Trade Agreement. It comes under review every five years ending in '2' and '7' so in 2027. It could be done earlier if parties agree. I expect Trump will say to Canada if you want no tariffs and free access than eliminate your 270% tariffs on dairy and similar high tariffs on poultry. Give us access to your Telecom and Banking industries. Fix your border. Something along these lines will play out in the next year or so.

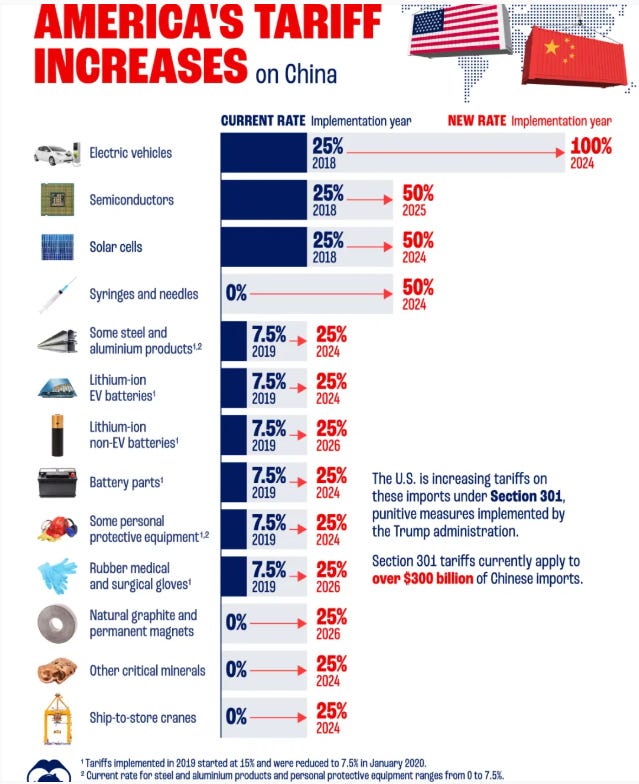

The other propaganda you hear from Canadian government and media is Trump is crazy, unfair, why is he only putting 10% on China? The above chart is of late 2024 and most goods in China already have 25% tariffs or more from the last time Trump was President. It is one policy Biden kept of Trumps. So most goods in China will now have 35% tariffs and higher. In the case of Chinese steel and aluminum, it will go from 25% to 50%. You can spend hours reading about the trade agreement on Government of Canada website.

This should come as no surprise for readers here as reported today, consumer prices rose 0.5% from December — the fastest pace since September 2023 — resulting in an annual inflation rate of 3% for the 12 months that ended in January. Narrative of inflation coming under control, blew up.

Economists were expecting Wednesday’s report to be fairly unexciting, with barely any change from December’s data. Instead, the January report came in hot pretty much across the board. “The long national nightmare of inflation isn’t over yet for consumers, businesses, and investors,” Chris Rupkey, chief economist at FwdBonds. Even core moved higher in January: It jumped 0.4% on a monthly basis, bringing the annual rate up to 3.3% from 3.2%.

Tariffs will also add to inflation but not all of it gets passed on to consumers. The last time Trump was president, tariffs implemented then did not increase inflation much if at all. It is hard to say how it will all filter through and it will take time. And concurrently there are forces at play that will reduce inflation. We could see inflation down to 2% in a year but unfortunately it will be caused by a recession, so in that case you still have stagflation. The policies that drove high immigration were inflationary and now are being reversed.

Ed Dowd explains: “What we are going to have going forward is the reversal of deficit government spending, which was juicing the economy with illegals. Some of them got jobs, but a lot of them got benefits. They got housing accommodations. The NGO system was flush with money to facilitate this massive, purposeful logistical operation.”

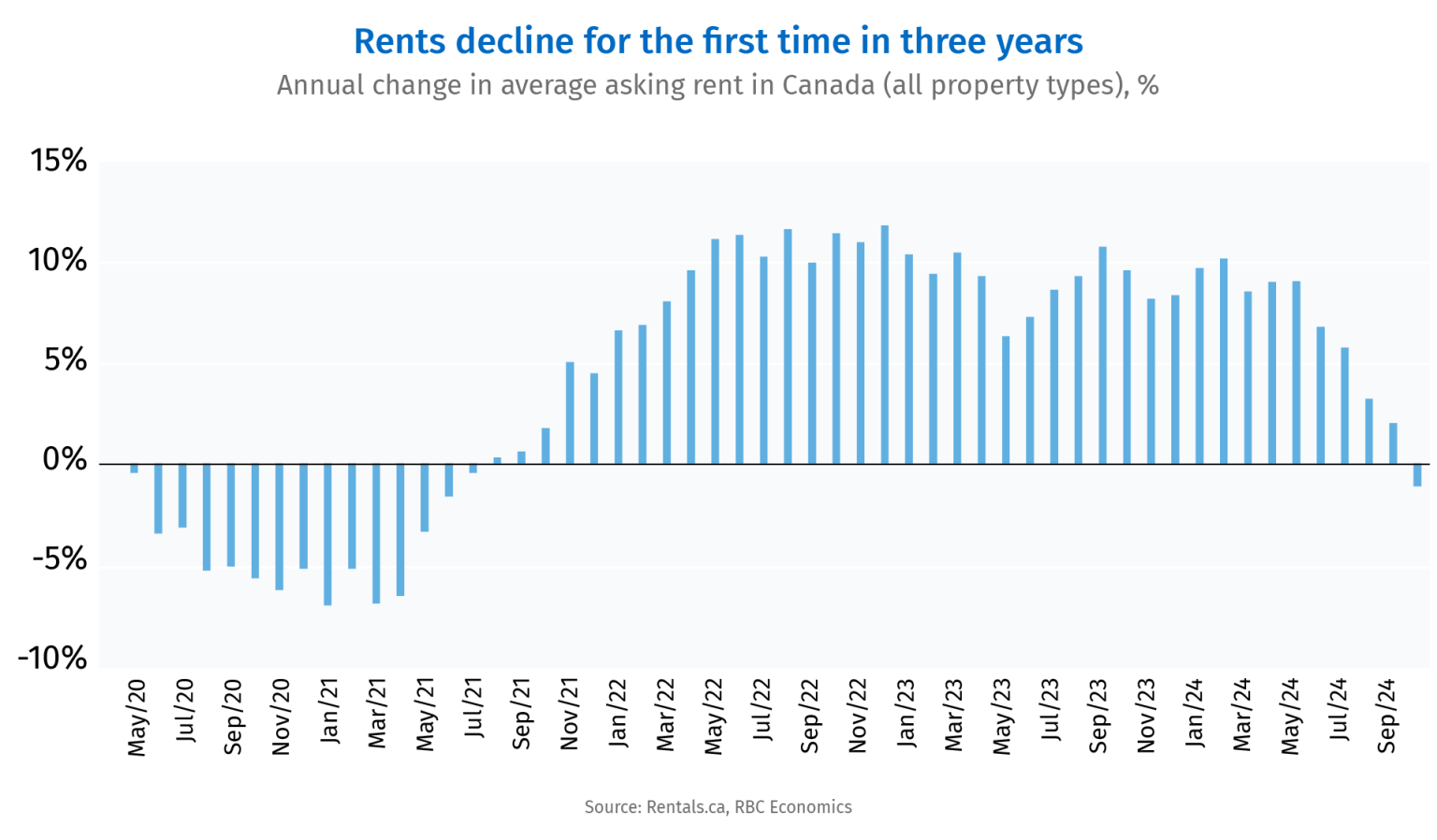

The immigration inflationary pressure was even greater in Canada compared to U.S. I talked about cracks in U.S. housing here and now we see downward movement on rent prices.

The median U.S. asking rent fell to $1,594 in December, its lowest level since March 2022 and down 6.2% from its record high of $1,700 in August 2022. When examined by square footage, median asking rent fell 1.9% year-over-year to $1.78. The drop comes after rents soared in the last few years as demand for housing grew.

The asking rent for units across Canada fell for the first time in three years in October with big declines seen in the largest and most expensive cities of Toronto and Vancouver—providing some relief to lease hunters where rent unaffordability has been crushing.

Asking rent for a two-bedroom unit was down $320 (-9.4%) in Toronto in October from the same month a year ago. Surrounding areas like Brampton (-$256) and Mississauga (-$111) also posted sizable declines after months of softening prices.

Canada’s most expensive rent market, Vancouver, saw an even larger $478 dip (-12% y/y) in asking rent and an outsized drop posted in neighbouring Burnaby (-$349). Still, at an average of $3,430 and $3,091 respectively, advertised rent in Toronto and Vancouver continues to represent roughly 40% of median household income in those cities.

A few factors are adding downward pressure to Canada’s rent market this year. For one, rental completions have ramped up significantly in recent quarters as construction projects that started some time ago reach the finish line. The number of purpose-built units started nearly quadrupled in the past decade, accelerating significantly since 2018 after the introduction of various government incentives. That’s added to the supply of available units, providing more choice to lease hunters.

The fall of rent prices is continuing from October 2024 above into 2025. The national rent report from Rentals.ca and Urbanation found the average monthly asking rent for all residential properties in January fell to $2,100, roughly a 4.4 per cent annual decline and a decrease of $96.

“The downward trend for rents in Canada accelerated during the first month of 2025,” said Shaun Hildebrand, Urbanation president. “Heightened downside risks for the economy, combined with declining international population inflows and multi-decade highs for apartment completions, suggest rents will continue to weaken in the months ahead.”

The Toronto condo market is in free fall so Toronto was also found to be home to the most drastic reduction in asking rents for shared accommodation, with the typical room in a shared space now going for $1,194, or 9 per cent cheaper than a year ago.

The majority of condo investors in the GTA are now losing money on new units, with mortgage payments paired with surging maintenance fees and property taxes outpacing the rent they can earn to float their purchase. At the same time, resale prices are plummeting so not easy to get out except with big losses. It was easy to see this coming when I called and talked about this with the housing bubble top in April 2022.

“ I expect in major Canadian city centres we could see condo prices rise while housing prices fall, sort of a rebalancing. However once the decline accelerates and the pin pricks the bubble, both will fall. Home prices in Toronto’s housing market fell in March 2022. The average sold price in the GTA was $1,299,894 for the month of March 2022, which is down from the $1,334,544 average home price seen in February 2022. This is just one month, but I suspect it is the start of a new trend.”

Horror stories from landlords who have been unable to hold delinquent tenants accountable through the province's failing Landlord and Tenant Board also aren't encouraging to anyone looking to rent a property out at the moment. I know a lot about this as my daughter's paralegal business focusing on the Landlord Tenant act is booming and has been since post Covid.

Cheap Gold Stocks and Analysts Love My Picks.

The Globe and Mail reports in its Wednesday edition that with increasing gold bullion prices, earnings per share expectations for miners have risen by 60 per cent and 80 per cent for 2025 and 2026 since April, 2024. The Globe's guest columnist Bhawana Chhabra writes that stock prices, however, have only increased by 25 per cent, matching the pace of gains in gold itself over the same period. With a forward price-to-earnings ratio of 12 times earnings and annualized earnings growth for the next three years forecast at 38 per cent, the PEG ratio (forward P/E to earnings growth) works out to be just 0.3 times. A PEG ratio of less than one is considered cheap, between one and two is considered reasonable and more than two is regarded as expensive. This all implies that precious metals miners are available at bargain basement prices.

National Bank Financial analysts predict a "mixed" earnings season for Canadian precious metals producers following the release of fourth quarter 2024 operating results. And increased ratings on:

They boosted their target for Iamgold, which they rate "outperform," to $13.50 from $12. Our buy price $3.51

They boosted their target for Calibre Mining, which they rate "outperform," to $4 from $3.40. Our buy price $1.63

They boosted their target for Kinross Gold (one of their top picks), which they rate "outperform," to $22 from $20. Our buy price $6.35

They boosted their share target for Pan American Silver, which they rate "outperform," to $47.25 from $45. Our buy price $22.85

They cut their share target for Aya Gold & Silver (which is one of their top pick), which they rate "outperform," to $20.75 from $21.25. Our buy price $11.43

RBC analysts continue to rate Alamos Gold "outperform." They boosted their share target to $27 (U.S.) from $25 (U.S.). Our buy price $12.43

Gold stocks are up today even with gold down some and markets tanking. The TSX Venture index is up a little with markets tanking. Perhaps we are seeing the first signs of the precious metal sector getting traction from other markets faltering.

Paid Advertisers at playstocks

All forecasts and recommendations are based on opinion. Markets change direction with consensus beliefs, which may change at any time and without notice. The author/publisher of this publication has taken every precaution to provide the most accurate information possible. The information & data were obtained from sources believed to be reliable, but because the information & data source are beyond the author's control, no representation or guarantee is made that it is complete or accurate. The reader accepts information on the condition that errors or omissions shall not be made the basis for any claim, demand or cause for action. Because of the ever-changing nature of information & statistics the author/publisher strongly encourages the reader to communicate directly with the company and/or with their personal investment adviser to obtain up to date information. Past results are not necessarily indicative of future results. Any statements non-factual in nature constitute only current opinions, which are subject to change. The author/publisher may or may not have a position in the securities and/or options relating thereto, & may make purchases and/or sales of these securities relating thereto from time to time in the open market or otherwise. Neither the information, nor opinions expressed, shall be construed as a solicitation to buy or sell any stock, futures or options contract mentioned herein. The author/publisher of this letter is not a qualified financial adviser & is not acting as such in this publication.